Navigating the New Era of ESG Reporting: From Voluntary to Mandatory

The landscape of ESG reporting is undergoing a fundamental transformation. What began as voluntary sustainability reporting has rapidly evolved into a complex ecosystem of mandatory disclosure requirements across major markets.

Governance

Microsoft turns to underground waste storage to offset AI's carbon toll

Microsoft has signed a long-term deal with Vaulted Deep to purchase carbon credits in an effort to offset emissions from its growing fleet of AI data centers. Vaulted's specialty? Human feces – or "excess organic material," as the official press release delic…

Strategic

UK Green Taxonomy Dies As Sustainability Regulations Face Global Pushback

HM Treasury announced they will not create a UK Green Taxonomy to define what actions are considered green, climate friendly, or other sustainability related claims.

Strategic

EPA Endangerment Finding

The 2009 EPA Endangerment Finding declared greenhouse gases a threat to public health and welfare, forming the legal basis for U.S. climate regulation under the Clean Air Act.

Strategic

Most Important KPIs for US Asset Managers

A comprehensive ESG investing dashboard should track portfolio carbon intensity, ESG integration, voting records, climate risk, sustainable offerings, diversity, engagement outcomes, and social and environmental impact to meet regulatory expectations and drive long-term value creation.

Governance

ESG Issue For PBMs

Pharmacy Benefit Managers (PBMs) operate at the financial heart of the U.S. prescription drug system, yet their opaque practices introduce significant ESG risks—especially regarding access to medicine, pricing transparency, and ethical governance. As regulators and standards bodies press for more accountability, stakeholders must consider PBMs' impact when disclosing under IFRS S1/S2, SASB, and GRI frameworks.

Governance

What are PBMs?

PBMs were intended to be cost-saving intermediaries, but their current structure incentivizes profit-maximizing behavior that often comes at the expense of patients, employers, and pharmacies. A growing body of evidence shows that PBM practices contribute to rising drug costs, reduced access, and market distortions. While some reforms are underway, systemic changes—including pricing transparency, realignment of incentives, and enhanced regulation—are essential to protect the public from ongoing abuses.

Environmental

Data Driven Decision-Making

Utilize advanced data analytics, real-time monitoring, and predictive intelligence to inform ESG strategy development, resource allocation, and performance optimization decisions.

Strategic

ESG Communication

Develop comprehensive communication strategies that foster transparent ESG dialogue, enable continuous stakeholder feedback, and drive ongoing improvement in sustainability performance.

Strategic

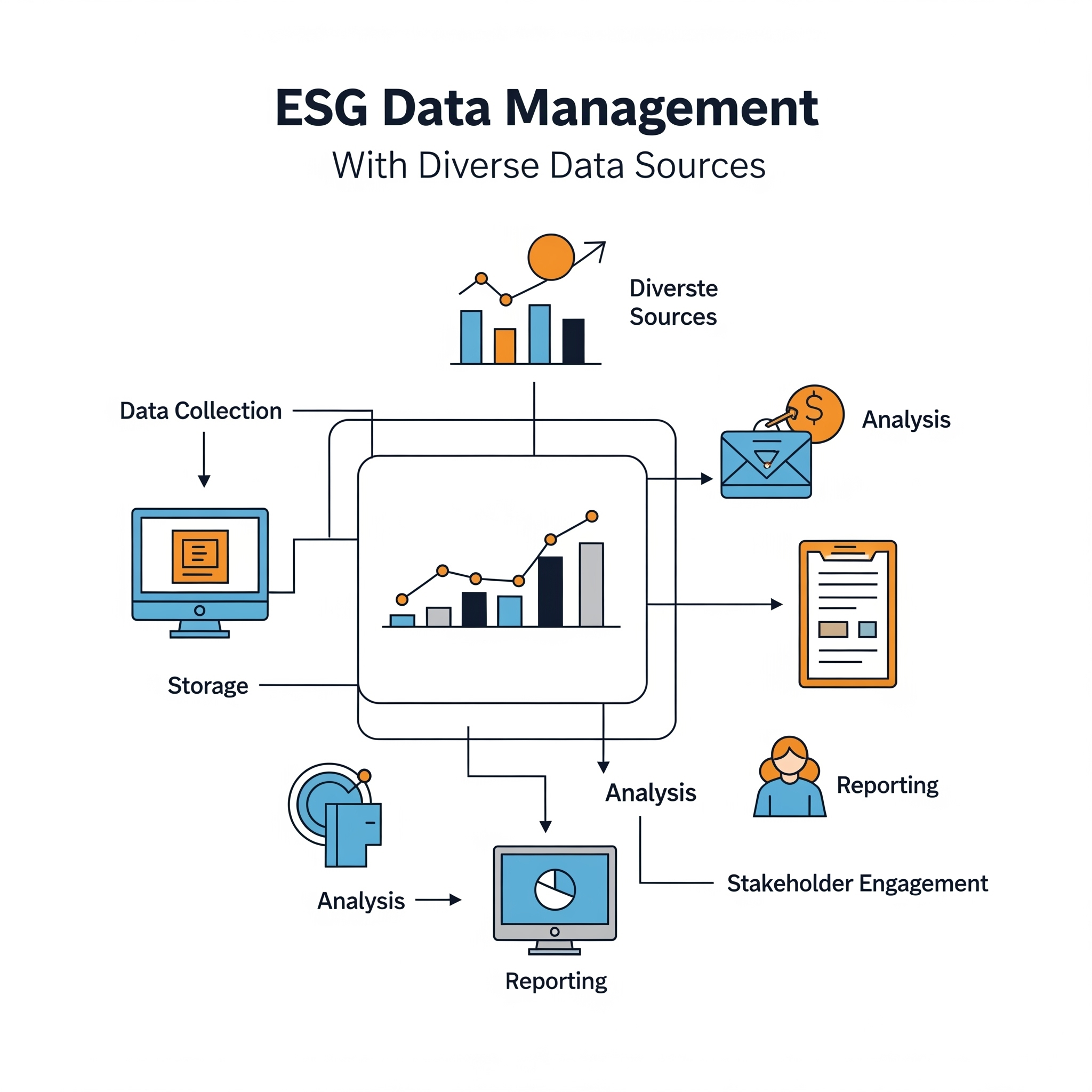

ESG Data

Establish comprehensive data collection, validation, and management systems to ensure accurate, reliable, and timely ESG performance measurement and stakeholder reporting.

Strategic

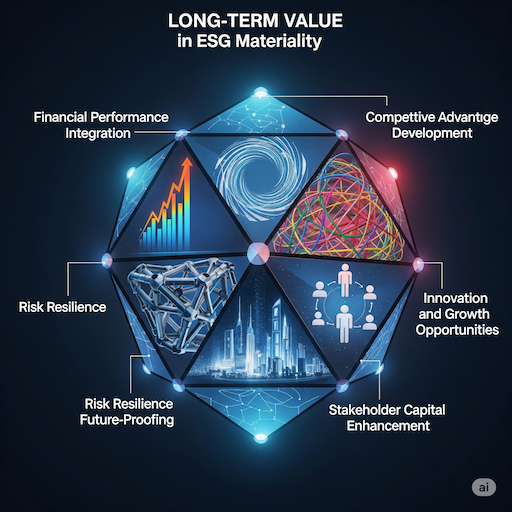

Long-Term Value

Align ESG materiality priorities with sustainable value creation strategies that drive competitive advantage, stakeholder returns, and business resilience over extended time horizons.

Strategic

Materiality Mapping

Systematically identify, assess, and prioritize ESG issues based on stakeholder importance and business impact to focus resources on the most material sustainability topics.

Governance

ESG Governance

Implement comprehensive governance frameworks that ensure effective ESG oversight, decision-making authority, and accountability at all organizational levels.

Governance

Cross-Functional Team

Establish diverse, cross-departmental teams to ensure ESG integration across all business functions and drive comprehensive sustainability outcomes.

Governance

Stakeholder Trust

Establish credibility and long-term relationships through transparent ESG practices and consistent communication with all stakeholders.

Governance

IRA Repeal Impacts

S&P Global Market Intelligence analysis reveals that repealing the Inflation Reduction Act would reduce US solar, wind, and battery capacity by 13-15% while increasing gas generation by 16%, cutting CO₂ emissions progress from 20% to just 11% below 2022 levels by 2035. Regional impacts vary dramatically: Texas uniquely benefits with lower energy prices, Florida suffers the worst outcomes with most renewables becoming uneconomical due to no renewable mandates, California faces the largest price increases, and New York must compensate for lost offshore wind capacity. The key finding is that states with strong Renewable Portfolio Standards fare much better than those relying on market economics alone, proving federal tax credits are crucial for clean energy deployment.

Strategic

Carbon Earnings at Risk

"Carbon earnings at risk" refers to the potential financial losses a company could face due to its greenhouse gas (GHG) emissions in a world where carbon is priced—either through carbon taxes, emissions trading systems (ETS), or regulatory penalties. It’s a form of transition risk under the broader category of climate-related financial risks (as outlined by the TCFD and increasingly by IFRS S2).

Strategic

Trust in Conflict and Mediation

Trust is essential for managing conflict effectively. High trust allows for easier conflict resolution, while low trust makes conflicts destructive and difficult to resolve. Ultimately, the level of trust shapes conflict dynamics, and rebuilding trust is often key to resolving disputes.

Strategic

René Girard

René Girard was a French thinker whose revolutionary mimetic theory uncovered how human desire, rivalry, and violence are intertwined—shaping culture, religion, and myth.

Strategic

Financed Emissions Example

Use emissions intensity to allocate emissions to Scope 3 Category 15.

Environmental

Financed Emissions

Scope3 Financed Emissions: Greenhouse gas emissions associated with a company's investments, lending, and financial activities, particularly in the context of their portfolio companies.

Emissions Allocation: The process of assigning emissions to a specific lender or investor based on their exposure to a portfolio company's emissions.

Environmental

Namibia Energy Use Per Capita

Average energy consumption per person each year.

Strategic

Methane

Methane is a simple hydrocarbon with the chemical formula CH₄. It’s made up of:

1 carbon (C) atom

4 hydrogen (H) atoms

Strategic

UN Global Compact

Corporate sustainability starts with a company’s value system and a principles-based approach to doing business. This means operating in ways that, at a minimum, meet fundamental responsibilities in the areas of human rights, labor, environment, and anti-corruption. Responsible businesses enact the same values and principles wherever they have a presence and know that good practices in one area do not offset harm in another.

Strategic

Theory of Change

A theory of change explains why we think certain actions will produce desired change in a given context.

Strategic

ESG Impacts of President Trump's Cost-Cutting Measures

An analysis of the potential ESG implications stemming from President Trump's proposed cost-cutting initiatives, including reductions in federal spending, regulatory changes, and their effects on environmental policies, social programs, and governance structures.

Strategic

What is Nuclear Fusion?

Fusion is the process of combining two or more atomic nuclei to form a heavier nucleus, releasing a tremendous amount of energy in the process. It is the same process that powers stars, including our Sun, and is considered one of the most promising sources of clean and virtually limitless energy.

Environmental

What Are Small Modular Reactors?

Small Modular Reactors (SMRs) are a type of nuclear reactor that are designed to be smaller, more flexible, and often more cost-effective than traditional large-scale nuclear power plants.

Environmental

What is Nuclear Energy?

Nuclear energy is a type of energy that is generated by harnessing the power of atomic reactions. It's a way to produce electricity without burning fossil fuels like coal, gas, or oil.

Environmental

CSRD Scope Considerations

Understand which companies fall under the CSRD after the 2025 simplifications, including new thresholds, reporting deadlines, and expanded scope for non-EU operations.

Governance

European Sustainability Reporting Standards (ESRS)

The European Sustainability Reporting Standards (ESRS) are a set of comprehensive guidelines created to support the Corporate Sustainability Reporting Directive (CSRD).

Governance

Emission Factors for Scope 2 Market-Based Method

The Scope 2 Market-Based Method for calculating greenhouse gas (GHG) emissions focuses on using emission factors that reflect the specific electricity purchases of an organization, rather than using the average emissions from the local grid (which is the approach for the Location-Based Method).

Environmental

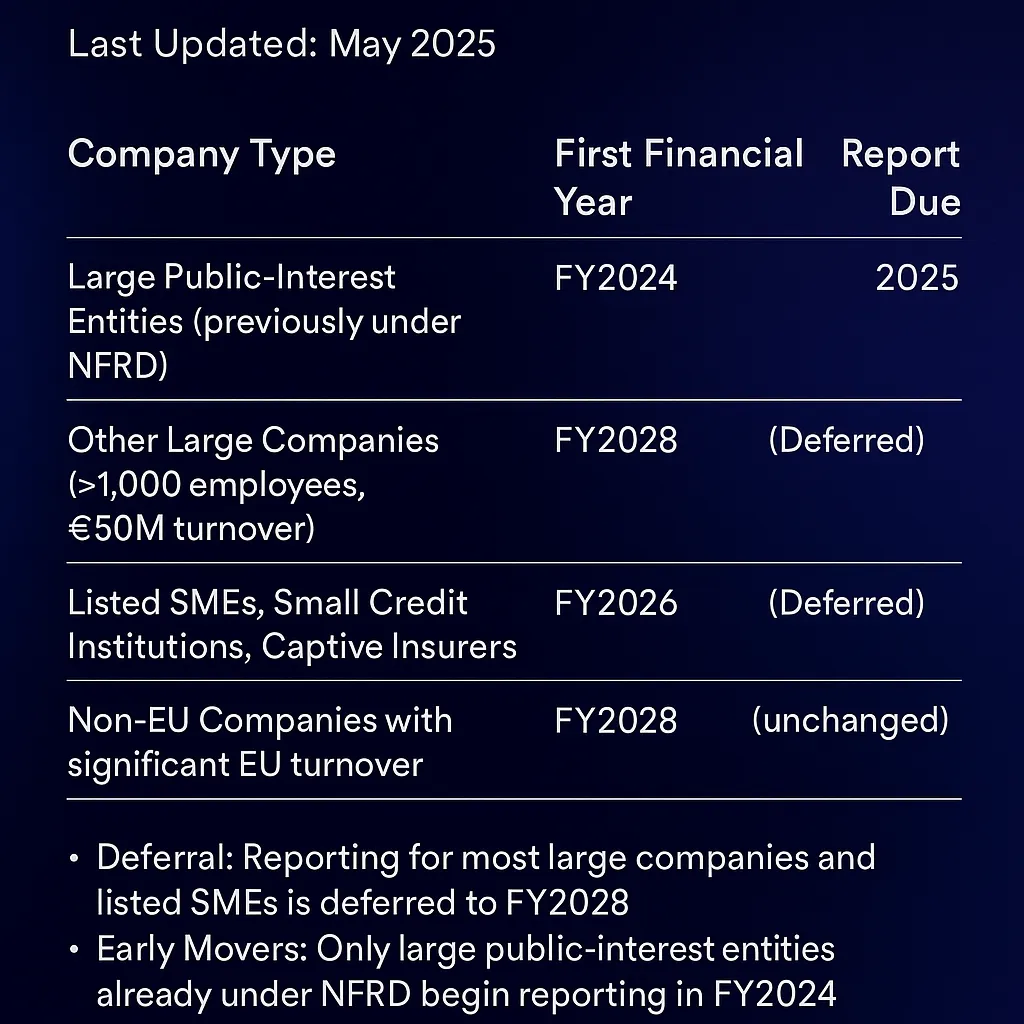

CSRD First-Time Reporting Timeline

Updated 2025 CSRD reporting timeline delays compliance for most companies until FY2028. This phased implementation supports SMEs and non-EU companies with extended preparation windows.

Governance

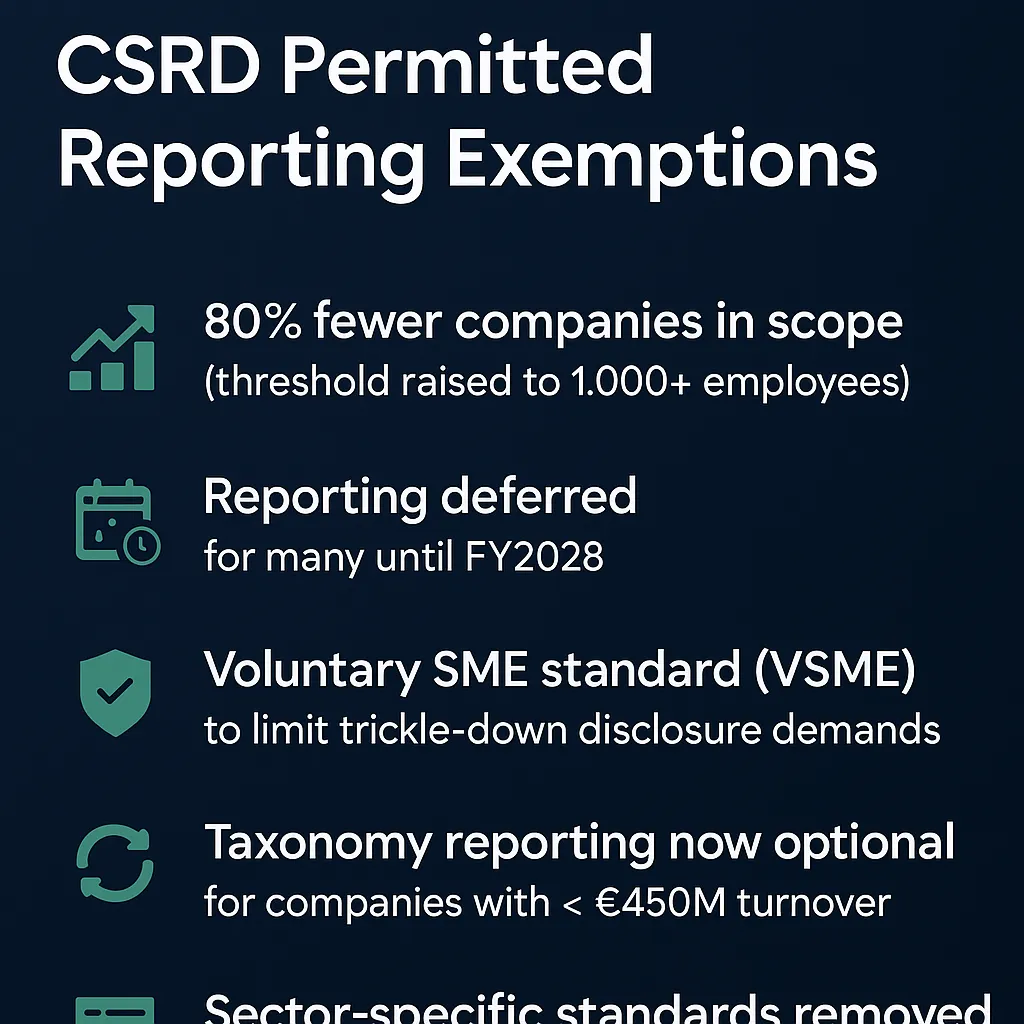

CSRD Permitted Reporting Exemptions

Updated CSRD guidance reduces scope by 80% and postpones reporting deadlines to FY2028. Introduces voluntary SME standards and simplified assurance rules.

Governance

Primary Climate Hazards

Primary climate hazards are extreme weather events and environmental changes intensified by climate change, posing significant risks to ecosystems, human health, and infrastructure.

Strategic

Phronesis

Phronesis, often translated as "practical wisdom," is a central concept in Aristotelian ethics, emphasizing the ability to make sound moral decisions in varying circumstances.

Strategic

How Multiphase Pumps Cut Emissions in Oil & Gas

Unlock efficient CO₂ and methane reduction with multiphase pumps—innovative tech for a cleaner oil and gas future.

Environmental

IMEO

Reducing methane emissions is the single fastest way to slow global warming as we decarbonize, but the world needs empirical data to enable climate action at scale. UNEP’s International Methane Emissions Observatory (IMEO) is harnessing this methane data revolution by putting open, reliable, and actionable data directly into the hands of individuals with the power to reduce emissions.

Environmental

Cutting Methane in Oil & Gas: Partnership 2.0.

The Oil & Gas Methane Partnership 2.0 (OGMP 2.0) is the United Nations Environment Programme’s flagship oil and gas reporting and mitigation programme. OGMP 2.0 is the only comprehensive, measurement-based reporting framework for the oil and gas industry that improves the accuracy and transparency of methane emissions reporting.

Environmental

WSJ Article - ESG is a Dirty Word

Many companies no longer utter these three letters: E-S-G. Following years of simmering investor backlash, political pressure and legal threats over environmental, social and governance efforts, a number of business leaders are now making a conscious effort to avoid the once widely used acronym for such initiatives.

Strategic

CHIPS and Science Act

The CHIPS and Science Act, also known simply as the CHIPS Act, is a U.S. federal law signed by President Joe Biden on August 9, 2022. The primary goal of the CHIPS Act is to bolster domestic semiconductor manufacturing, enhance supply chain resilience, and promote technological research and innovation in the United States.

Governance

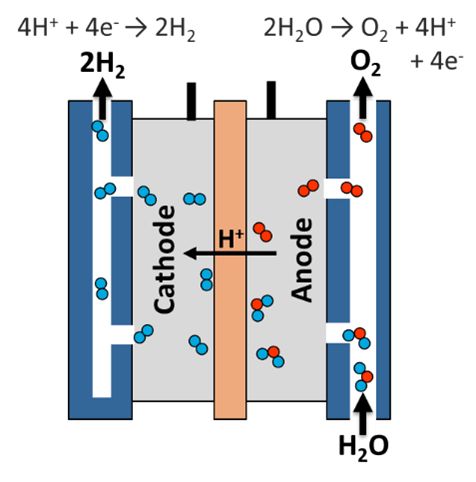

How a Hydrogen Fuel Cell Works

A hydrogen fuel cell is a device that converts hydrogen into electricity through a chemical reaction, with water and heat as the only byproducts. It is a clean energy technology that can power vehicles, buildings, and even portable devices without emitting harmful pollutants or greenhouse gases.

Environmental

Measuring Double Materiality: Focus on Governance Impact

Governance impact in the context of double materiality focuses on how a company’s governance structures influence both its financial performance and its broader societal impact. This approach requires organizations to evaluate both how governance practices affect their bottom line and how they impact stakeholders such as employees, shareholders, and the community.

Governance

Measuring Double Materiality: Focus on Social Impact

Social impact in the context of double materiality refers to how a company’s operations affect people and communities. This includes direct and indirect consequences of business activities on employees, consumers, local communities, and society at large.

Governance

Measuring Double Materiality: Focus on Water Impact

Hypothetical beverage company called "FreshDrink Co." Financial materiality (impact on the company):

Climate change is causing water scarcity in regions where FreshDrink Co. sources its water. This scarcity could lead to increased water costs and potential supply disruptions, directly affecting the company's financial performance and long-term viability.

Environmental and social materiality (impact of the company):

FreshDrink Co.'s water usage in water-stressed areas may deplete local water resources, affecting the surrounding ecosystems and communities' access to clean water.

Governance

Diversity Washing

Diversity washing, similar to greenwashing, refers to the practice of companies or organizations making superficial or deceptive claims about their commitment to diversity and inclusion without taking meaningful action. It involves projecting an image of supporting diversity, equity, and inclusion (DEI) while not implementing substantive changes to foster an inclusive workplace or culture. This practice can mislead stakeholders—employees, customers, and investors—about the organization's true efforts regarding diversity.

Social

Green Washing

Greenwashing is the practice of making false or misleading claims about the environmental benefits or sustainability of a product, service, or company. This can include exaggerating or fabricating a product's eco-friendliness, hiding its negative environmental impacts, or making unsubstantiated claims about its sustainability.

Governance

Texas’s 2021 Anti-ESG Law

Texas’s 2021 Anti-ESG Law and 2022 Blacklist refer to legislative and regulatory actions taken by the state of Texas to counteract what it views as discriminatory practices against the oil and gas industry by financial institutions that follow environmental, social, and governance (ESG) principles.

Strategic

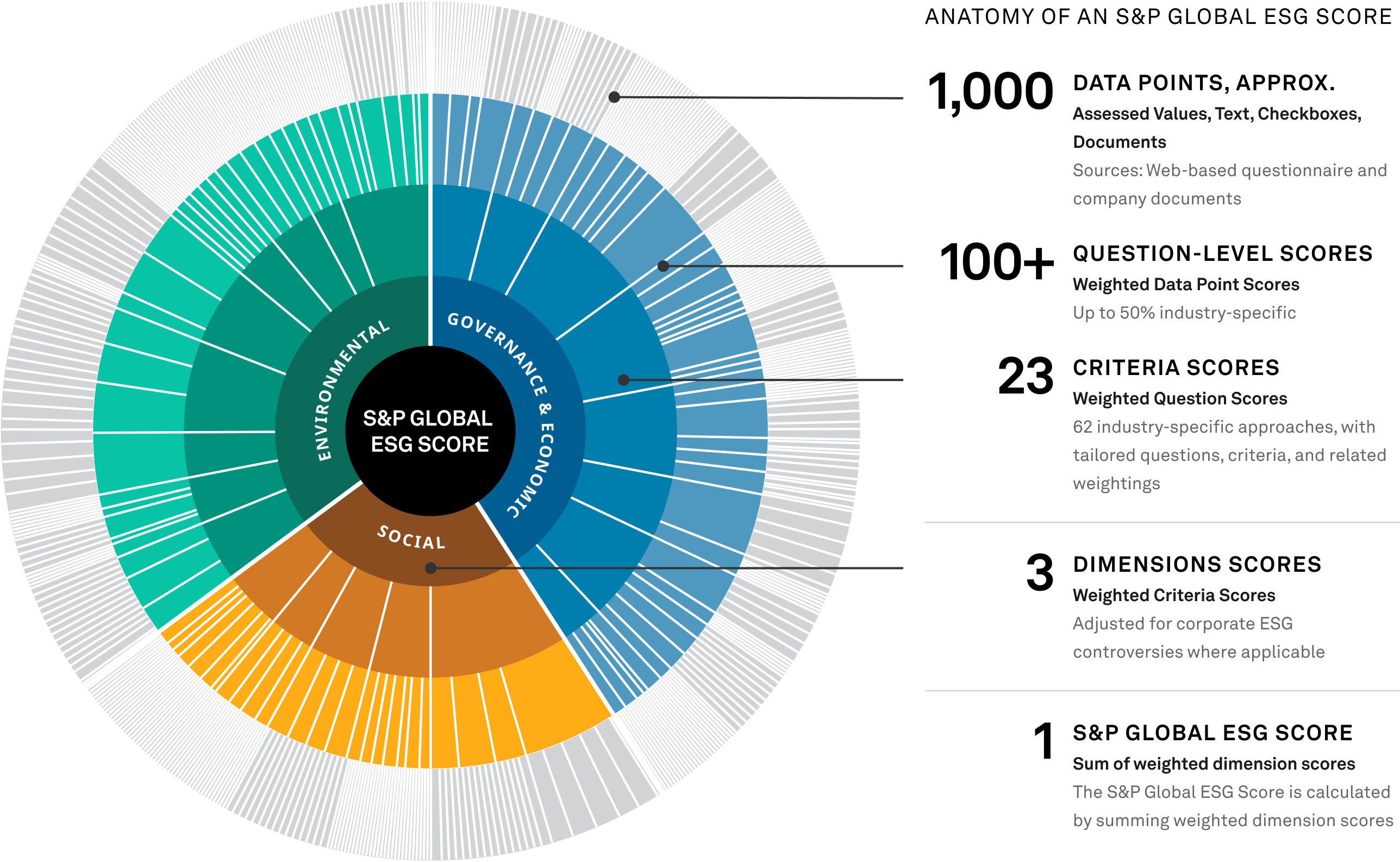

S&P Global CSA Score

The S&P Global CSA Score is the S&P Global ESG Score without the inclusion of any modeling approaches. The graphic below visualizes the CSA. The size of the segments reflects the financial materiality assigned at each level as well as the weight applied in the score aggregation process.

Governance

Global Industry Classification Standard (GICS®)

The Global Industry Classification Standard (GICS®) was developed in 1999 by S&P Dow Jones Indices and MSCI. The GICS methodology aims to enhance the investment research and asset management process for financial professionals worldwide. It is the result of numerous discussions with asset owners, portfolio managers, and investment analysts around the world. It was designed in response to the global financial community’s need for accurate, complete, and standard industry definitions.

Strategic

ISO 37000 Governance of Organizations

ISO 37000:2021 Governance of organizations — Guidance provides organizations and their governing bodies the tools they need to govern well, enabling them to perform effectively while behaving ethically and responsibly.

Governance

Compliance vs. Voluntary Carbon Market

Carbon Markets:

The compliance carbon market is regulated by laws that enforce emissions reductions, such as the EU ETS and California’s cap-and-trade program. Companies buy or sell carbon credits based on their emissions. The voluntary carbon market, driven by corporate net-zero goals, operates independently but is rapidly expanding. Transactions are increasingly conducted on digital exchanges, with blockchain technology playing a growing role in trading carbon credits.

Environmental

Carbon Intensity Measures

Measures for carbon intensity can vary based on the industry and the specific focus of the measurement. Here are some of the most common measures for carbon intensity.

Environmental

European Financial Reporting Advisory Group (EFRAG)

EFRAG (European Financial Reporting Advisory Group) is an independent, non-profit organization that provides advice and support to the European Union (EU) on financial reporting and accounting matters.

Governance

Benchmarking

Benchmarking ESG peers enhances a company's sustainability efforts by identifying best practices, improving performance, ensuring regulatory compliance, and increasing transparency.

Governance

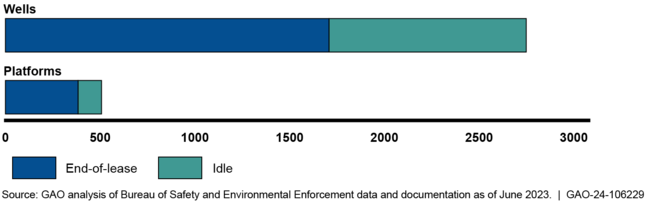

Offshore Oil and Gas Decommissioning

Oil and gas companies with offshore infrastructure must decommission it when it's no longer useful—by plugging wells and removing platforms within set deadlines. As of June 2023, more than 2,700 wells and 500 platforms were overdue for decommissioning in the Gulf of Mexico. Delays can increase environmental, safety, and financial risks. For example, delays could indicate that companies are in financial trouble and may leave the government to pay for decommissioning. The Department of the Interior only holds about $3.5 billion in bonds from companies to cover a potential cost of $40-$70 billion.

Strategic

Carbon Border Adjustment Mechanism (CBAM)

The Carbon Border Adjustment Mechanism (CBAM) is a proposed policy instrument designed to address the issue of carbon leakage in the European Union's (EU) climate change mitigation efforts.

Environmental

SEC Final Climate Disclosure Rule

The final rule adopted on March 6, 2024, requires public companies to disclose information in three key areas: (1) climate-related financial risks, (2) GHG emissions, and (3) any climate-related targets or transition plans.

Governance

CDP

CDP is a not-for-profit charity that runs the global disclosure system for investors, companies, cities, states, and regions to manage their environmental impacts. The world’s economy looks to CDP as the gold standard of environmental reporting, with the richest and most comprehensive dataset on corporate and city action.

Strategic

European Sustainability Reporting Standards (ESRS)

The European Sustainability Reporting Standards (ESRS) are a set of standards developed under the mandate of the Corporate Sustainability Reporting Directive (CSRD) by the European Financial Reporting Advisory Group (EFRAG). The ESRS aims to provide a unified framework for sustainability reporting within the European Union, enhancing the consistency, comparability, and reliability of sustainability information provided by companies.

Governance

IDD (Insurance Distribution Directive)

The IDD is about setting EU-wide rules for selling insurance products. It came into effect in October 2018.

Governance

MiFID II

MiFID II stands for the "Markets in Financial Instruments Directive II." It's a law in the European Union (EU) that regulates companies providing services linked to financial instruments (like stocks, bonds, units in collective investment schemes, and derivatives) and the places where those instruments are traded (like stock exchanges). Think of it as a set of rules to make financial markets more transparent, safe, and fair for everyone, especially for individual investors.

Governance

2020 UK Stewardship Code

The responsible allocation, management, and oversight of capital to create long-term value for clients and beneficiaries, leading to sustainable benefits for the economy, the environment, and society

Governance

S&P Global ESG Score

Scores are based on the Corporate Sustainability Assessment (CSA), previously known as the DJSI questionnaire.

Governance

Refinitiv ESG Score

ESG scores from Refinitiv are designed to transparently and objectively measure a company's relative ESG performance, commitment and effectiveness across 10 main themes (emissions, environmental product innovation, human rights, shareholders, etc.) based on publicly-reported data.

Governance

Bloomberg's ESG Disclosure Score

Bloomberg's ESG Disclosure Score is a rating system that measures the level of transparency and disclosure of a company's environmental, social, and governance (ESG) practices.

Governance

Bloomberg Environmental and Social (ES) Score

Bloomberg's Environmental and Social (ES) Scores are ratings that measure companies' environmental and social performance.

Governance

ISS Governance Quality Score

The ISS Governance Quality Score uses a numeric, decile-based score that indicates a company’s governance risk across four categories.

Governance

MSCI ESG Rating

An MSCI ESG Rating is designed to measure a company’s resilience to long-term, industry material environmental, social and governance (ESG) risks.

Governance

ISS ESG Corporate Rating

The ISS ESG Corporate Rating assesses a company's management of ESG issues on the basis of up to 100 rating criteria, based on the level of materiality to the company's sector.

Governance

Bloomberg Board Governance Score

Bloomberg's Board Governance Score ranks is a rating system that measures the diversity and inclusivity of a company's board of directors.

Governance

SEC Climate-Related Disclosures: Sunshine Meeting

Sunshine Meeting on Climate-Related Disclosures Announced by the SEC The Securities and Exchange Commission (SEC) has announced a Sunshine Meeting on Climate-Related Disclosures, which will be held on the SEC.gov website at 9:45 AM (ET) on Tuesday, March 6. This open meeting aims to discuss the SEC's ongoing efforts to enhance climate-related disclosures for publicly traded companies.

Environmental

Final Investment Decision (FID)

FID stands for Final Investment Decision. It's a key phase in the capital project planning process when the decision to make major financial commitments is taken. In energy, FID is the final step in determining whether to move forward with the construction of an infrastructure project. In exploration, FID costs are those directly related to the discovery of oil or another commodity.

Strategic

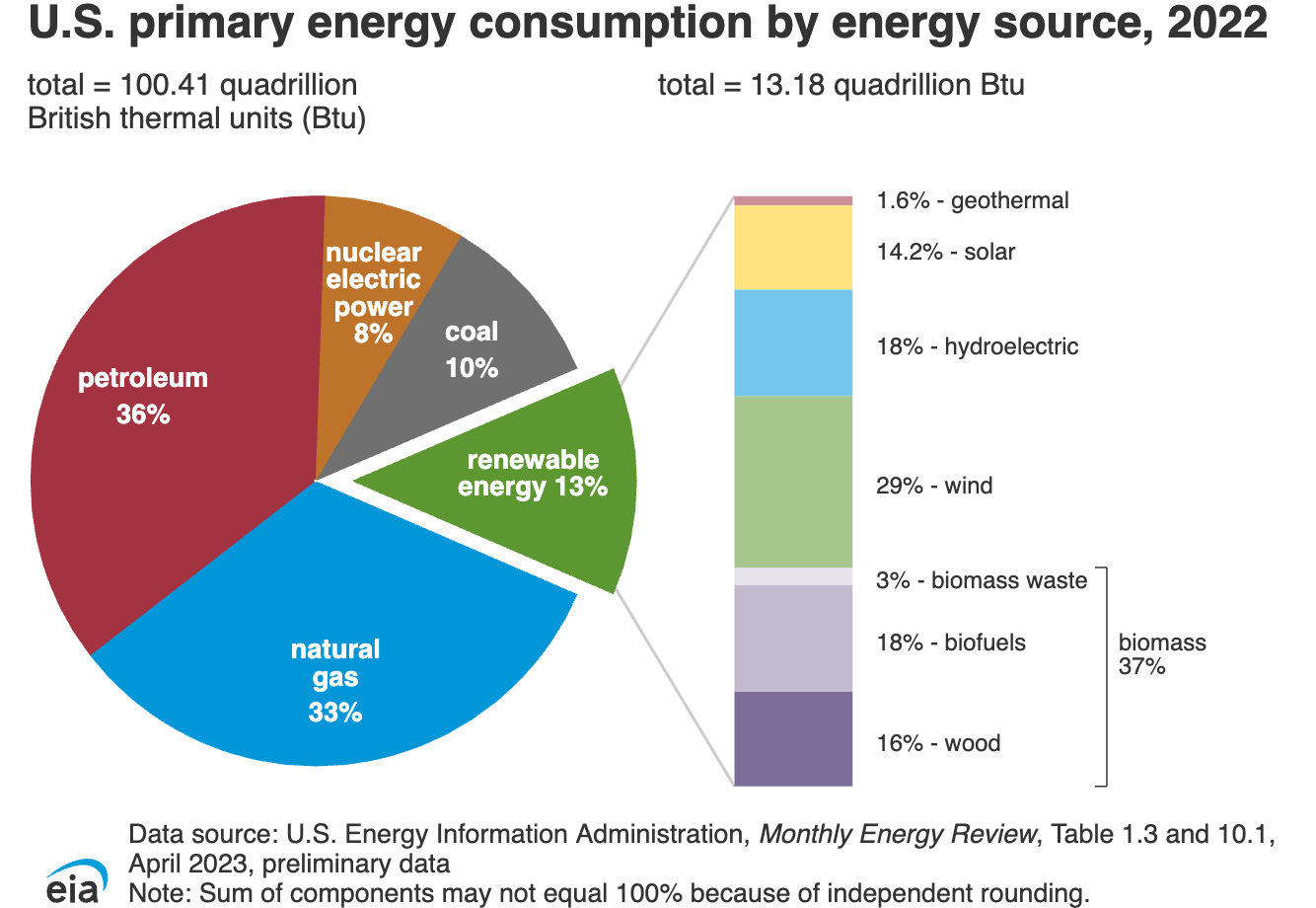

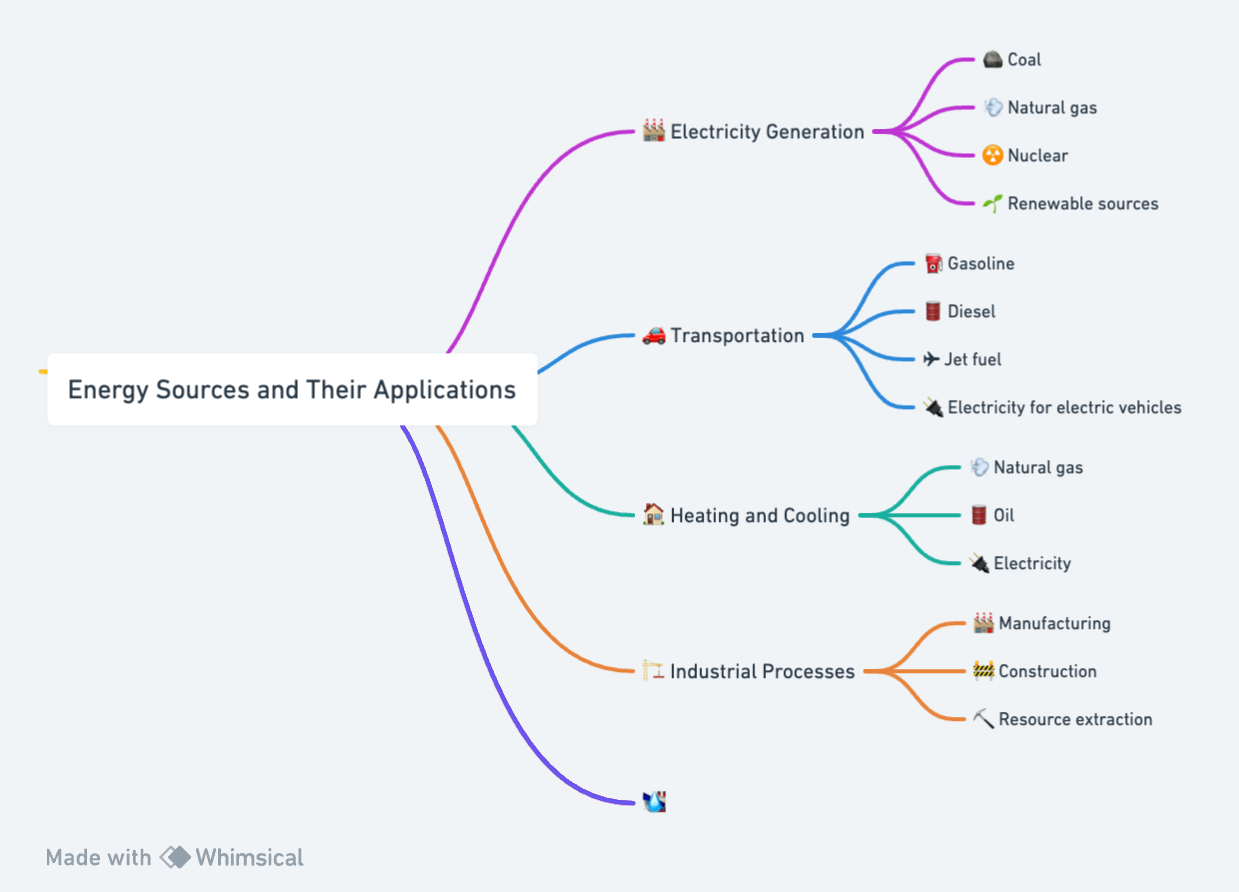

Energy Consumption by Energy Source

Total energy consumption by the end-use sectors includes their primary energy use, purchased electricity, and electrical system energy losses (energy conversion and other losses associated with the generation, transmission, and distribution of purchased electricity) and other energy losses.

Environmental

What is Energy Consumption

Energy consumption refers to the total energy used by individuals, businesses, industries, transportation, and every aspect of society.

Environmental

ISSB and SASB

The International Sustainability Standards Board (ISSB) and the Sustainability Accounting Standards Board (SASB) represent complementary facets of the global effort to standardize sustainability reporting. The ISSB provides a global baseline for sustainability and climate-related disclosures through its S1 and S2 standards, focusing on general sustainability issues and specific climate impacts, respectively. These standards aim to enhance transparency, consistency, and comparability in reporting across all sectors. SASB, now integrated under the IFRS Foundation alongside ISSB, complements this by offering industry-specific frameworks that identify material sustainability issues relevant to different sectors, providing detailed metrics for companies to measure and report their sustainability performance. Together, ISSB's broad principles and SASB's detailed industry guidance aim to streamline sustainability reporting, making it more relevant and actionable for stakeholders worldwide.

Governance

European Sustainability Reporting Standards

The ESRS standards are reporting standards for sustainability within the EU. The ESRS standards are an integral part of the CSRD, the Corporate Sustainability Reporting Directive of the European Parliament and the Council. This means that the ESRS reporting standards are mandatory. The adoption of the first set of 12 standards by the Commission is considered a significant step to promote sustainable practices and transparency in companies and to contribute to their comparability. This is because the new reporting requirements herald major changes in sustainability reporting and these will affect around 50,000 companies based in the EU. However, subsidiaries, branches abroad and companies that carry out a large part of their business activities in the EU area may also be indirectly affected, which is why the scope of impact can be significantly broader.

Governance

West Virginia v. EPA

The Supreme Court limited the EPA's power to regulate power plant emissions by striking down the Clean Power Plan due to lack of clear Congressional authorization, potentially impacting future climate change regulations and agency power in general.

Environmental

IFRS S2

The objective of IFRS S2 is to require an entity to disclose information about its climate-related risks and opportunities that is useful to users of general-purpose financial reports in making decisions relating to providing resources to the entity.

Governance

IFRS S1

IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information provides a set of disclosure requirements designed to enable companies to communicate to investors about the sustainability-related risks and opportunities they face over the short, medium, and long term.

Governance

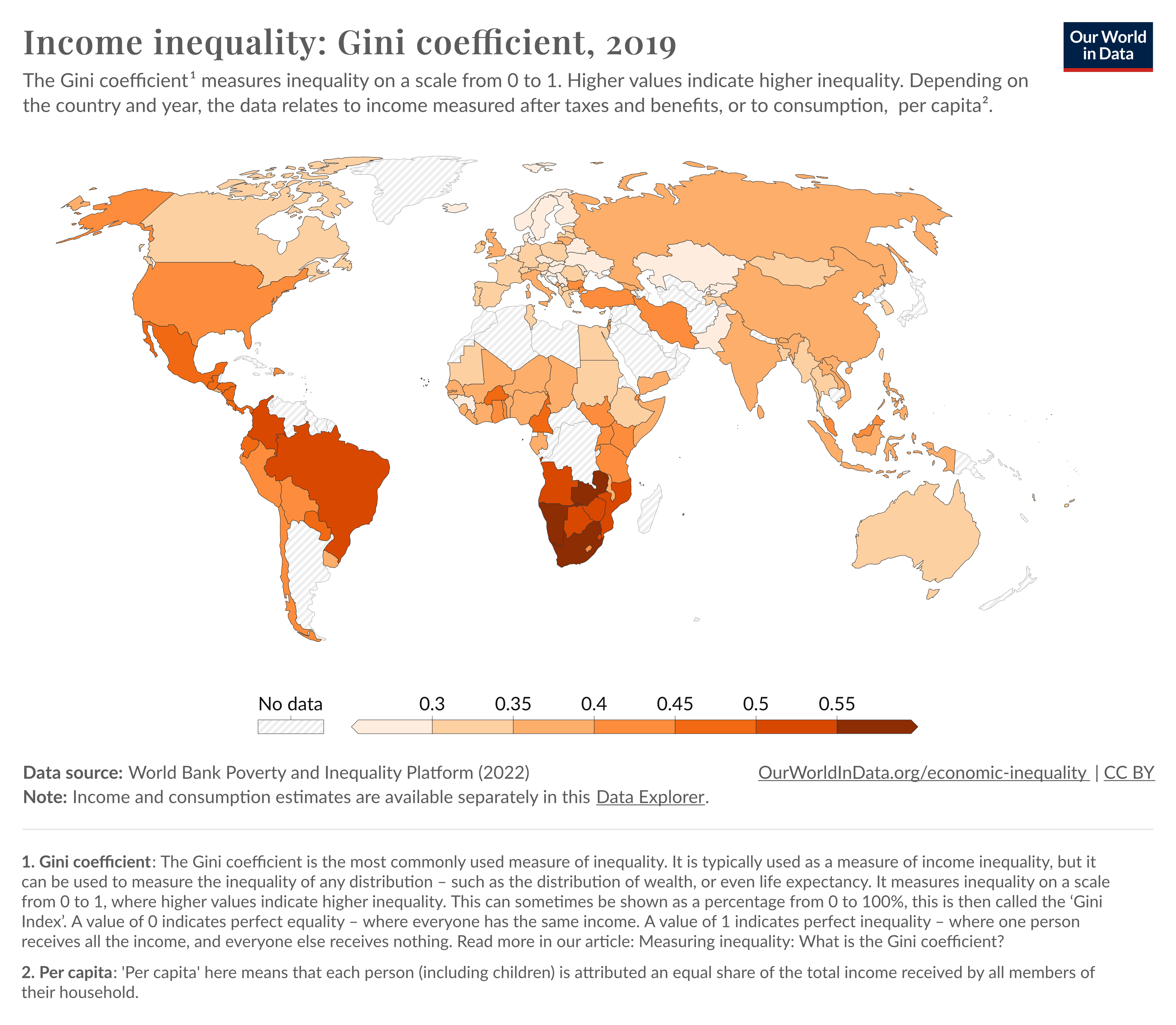

Gini Index

The Gini index measures the extent to which the distribution of income or consumption among individuals or households within an economy deviates from a perfectly equal distribution. A Gini index of 0 represents perfect equality, while an index of 100 implies perfect inequality.

Social

Transition Plan Taskforce

HM Treasury launched the Transition Plan Taskforce (TPT) in April 2022 to develop the gold standard for private sector climate transition plans.

Environmental

Integrated Reporting Framework

The Integrated Reporting Framework defines integrated reporting as ‘a process founded on integrated thinking that results in a periodic integrated report by an organisation about value creation over time and related communications regarding aspects of value creation.’

Governance

Africa

Population (2022, World Bank) 1.3 billion

GDP (2020, World Bank) 2.39 USD trillion

CO2 Emission (2020, EDGAR) 1 384,72 Mton

Electrification rate (2020, World Bank) 55.94 %

Installed Renewable Energy Capacity (2021, IRENA) 55.2 GW

Strategic

NZE

The Net Zero Emissions by 2050 Scenario (NZE Scenario) is a normative scenario that shows a pathway for the global energy sector to achieve net zero CO2 emissions by 2050, with advanced economies reaching net zero emissions in advance of others.

Environmental

Carbon Dioxide Removal

Carbon dioxide removal (CDR), often referred to as "negative emissions technologies," encompasses methods and technologies aimed at actively removing and sequestering carbon dioxide (CO₂) from the atmosphere.

Environmental

SASB Taxonomy

The SASB Taxonomy was designed for companies to report their ESG information following SASB Standards in a structured, machine-readable data format (i.e., XBRL) to the investor and analyst community and other companies’ non-financial information users.

Governance

XBRL

eXtensible Business Reporting Language is an open international standard for digital business reporting. The SASB Taxonomy was designed for companies to report their ESG information following SASB Standards in a structured, machine-readable data format (i.e., XBRL) to the investor and analyst community and other companies’ non-financial information users.

Governance

IFRS Foundation

The IFRS Foundation is a not-for-profit, public interest organization established to develop high-quality, understandable, enforceable, and globally accepted accounting and sustainability disclosure standards. Our Standards are developed by our two standard-setting boards, the International Accounting Standards Board (IASB) and Ithe International Sustainability Standards Board (ISSB).

Governance

SFDR Article 8

An Article 8 Fund under SFDR is defined as “a Fund which promotes, among other characteristics, environmental or social characteristics, or a combination of those characteristics, provided that the companies in which the investments are made follow good governance practices.”

Strategic

Carbon Intensity

Carbon intensity refers to the amount of carbon dioxide (CO2) emissions produced per unit of energy or economic output. It is a critical metric used to understand the environmental impact of various activities, sectors, or industries, and it helps to track progress in reducing greenhouse gas emissions over time.

Environmental

Sustainable Aviation Fuel (SAF)

Sustainable aviation fuel is a type of jet fuel formulated to have a reduced impact on the environment compared to conventional jet fuels. The primary goal of developing SAFs is to minimize the carbon footprint of aviation, which is responsible for a significant portion of global greenhouse gas emissions.

Environmental

Green Hydrogen

Green hydrogen is hydrogen produced using renewable energy or from low-carbon power. It is a clean-burning fuel that produces no emissions when used. Green hydrogen is produced by splitting water molecules into hydrogen and oxygen using an electrical current. The electricity can be generated from solar, wind, or other renewable sources.

Environmental

Emotional Intelligence (EQ)

Emotional Intelligence (EI or EQ, which stands for Emotional Quotient) refers to a person's ability to recognize, understand, manage, and effectively use their own emotions and recognize, understand, and influence the emotions of others. It involves a set of emotional and social skills critical for building and maintaining healthy relationships, both personally and professionally.

Strategic

Double Materiality

Double materiality suggests that companies should assess the impact of external environmental and social factors on their operations (external materiality) and evaluate the impact of their activities on the external environment and society (internal materiality).

Governance

Strategic Planning

Strategic planning refers to an organization's process of defining its direction and making decisions on allocating its resources to pursue this strategy. This typically includes developing the organization's vision, mission, objectives, and strategies to achieve them over time.

Environmental

Materiality

The International Accounting Standards Board (IASB) state that “information is material if omitting, misstating or obscuring it could reasonably be expected to influence the decisions that the primary users of general purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity.”

Strategic

FSB

The Financial Stability Board (FSB) is an international body that monitors and makes recommendations about the global financial system. It was established in 2009 by the G20 countries in response to the global financial crisis. The FSB's primary mandate is to promote financial stability by coordinating and enhancing the effectiveness of regulatory, supervisory, and other financial sector policies.

Strategic

Scope 3 Emissions: Employee Drive to Work

The emissions resulting from employees driving to work generally fall under scope 3 emissions rather than scope 1 emissions.

Environmental

EROI

Metric used to assess the energy efficiency and viability of an energy source or energy-producing process. EROI measures the ratio between the amount of usable energy acquired from a particular energy source and the amount of energy invested to obtain, produce, or harness that energy.

Environmental